“There’s no confirmation yet” that veterans’ data was leaked by the ransomware attack, according to the VA secretary, but the department is proactively alerting millions of veterans and beneficiaries to be safe.

The board will be made up of 22 representatives from private sector, government and academia and will advise Secretary Mayorkas on risk mitigation for AI in critical infrastructure.

As organizations recognize the important role of field services such as repairs and maintenance in delivering exceptional service, there's an increasing demand for solutions.

The move to allow federal employees to telework while overseas with their service member spouses is part of a larger effort to boost recruitment of military spouses.

New legislation attempts to improve NASA’s Advanced Capabilities for Emergency Response to Operations program so firefighters can more effectively use drones.

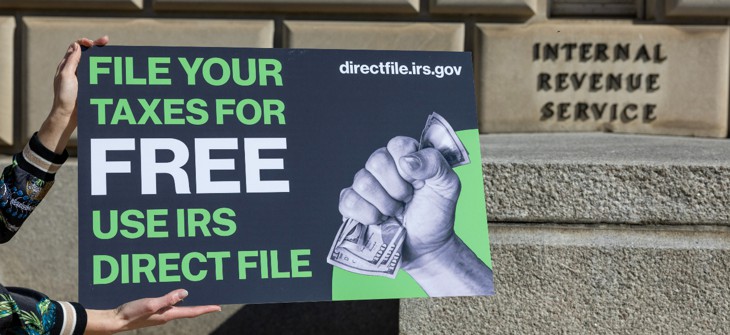

COMMENTARY | The Direct File pilot was a landmark event for the tax system and a victory for the civic technology movement. Now its time to make the program available to all taxpayers on a permanent basis.

Nick is renowned for mentoring an up-and-coming generation of government tech and policy talent. One supported said he's, “one of the first lifelines I call when I have a hard problem.”

The GSA chief information officer has seen the pace of change accelerate dramatically inside of government, especially recently with hard pivots on cybersecurity, customer experience, digital identity, cloud adoption and more.

The AI Corps program — modeled after the White House’s U.S. Digital Service — is intended to bring teams of experts to bear on the agency’s most critical mission needs.

Scientists and engineers with the space agency were able to successfully repair an issue in one of the probe’s onboard computers from over 15 billion miles away.

The Plain Language in Contracting Act would require agencies to use easy-to-understand language for certain procurement notices pertaining to small businesses.

COMMENTARY | Exciting advancements are ahead for the federal government by tapping generative AI, from streamlined operations to improved national security

A new request for information issued by the Department of Commerce asks for expert commentary on how the agency can better structure and disseminate its publicly available data.

The Department of Veterans Affairs said the ransomware attack impacted just over 40,000 veterans’ prescription orders but that it moved to quickly fill the requests.

.png)